Congratulations! you have made the decision to buy a resale flat by investing your life’s savings.

In the case of a property being bought from a builder, the registration process is typically guided by the builder’s legal team. But if one is buying a resale flat, at a lot of times seller or buyer aren’t well versed with the documents that are needed or how the whole process works. As part of this post, we are trying to give an overall picture of the process and different aspects of buying a flat as well as key things to know as a buyer.

1. Property Documents:

As soon as you finalize a property based on your requirements and growth aspects, it is prudent on buyer’s part to collect the following documents from seller for verification.

- Mother Deed

- Sale Deed

- Encumbrance certificate

- Tax Paid receipt

- Khata certificate & Extract

- Occupation Certificate

- Aadhar & PAN

2. Property Verification

Verify above-listed documents from a real estate lawyer. This is to ascertain the legal ownership of the property, tax liabilities with the property and to ensure that it is complying with the various regulations.

If you are opting home loan, your bank might verifies the documents

3. Sale Agreement

Property Sale Agreement is probably the most important document in the whole chain because even sale deed is executed based on terms covered under sale agreement as well as is legally binding. Sale agreement covers various aspects of the sale such as Indemnity Clauses, agreed cost, advance paid, Penalty clause, Right to call-off the deal, the procedure to be followed in case of default by either party, losses or obligations to be covered by buyer or seller etc. In case the agreement is not well drafted, it may allow one of the parties to breach the agreement and still get away with it.

Since even sale deed is executed based on terms & conditions agreed upon in the sale agreement; hence it is all the more important to have an expert drafted and thoroughly vetted sale agreement.

Below is the image of sale agreement draft

Seller and buyer signs all the pages of sale agreement. Two witnesses signs at last page of sale agreement.

4. Sale Agreement Adjudication:

If you are opting home loan to finance your property purchase, should adjudicate sale agreement in sub-registrar office, the adjudication cost is 0.5% of buying price or guidance value, whichever is higher.

(Guidance value is the minimum amount for which a property can be registered hence property would not be registered lower than the guidance value fixed by department of stamp & registration of your locality.)

Sale agreement after adjudication looks like below image

5.Home Loan

Home loan process can be triggered with the bank. The first step in securing a home loan is to get the loan sanctioned for which bank would need to look at the income proofs, property marketability and the credit score of the buyer including security or guarantor documents (some of this might be bank specific). The cheque or DD of the loan amount is issued in name of seller and once the property is registered original copies would be deposited with bank including registered sale deed.

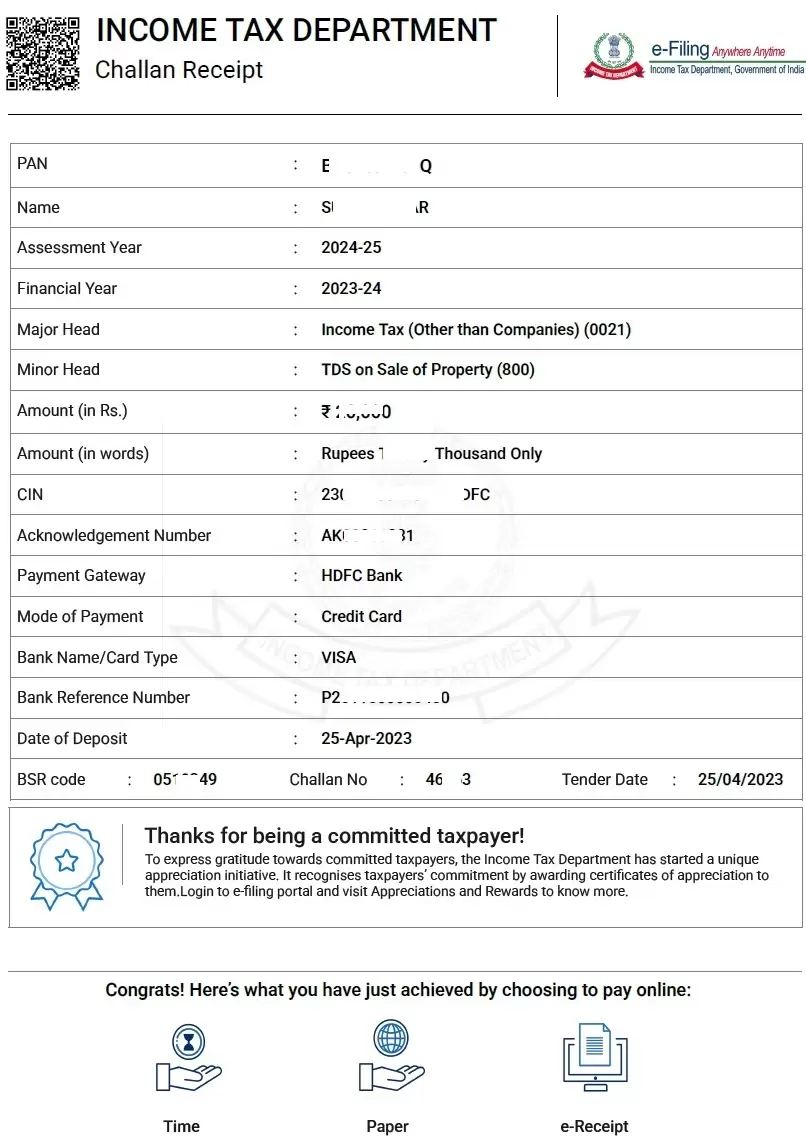

6. TDS (Tax Deducted at Source):

Who Pays TDS:As per the government regulation, the buyer responsible to deduct the TDS and not the seller. If the buyer does not discharge the duty of TDS payment, buyer can be penalized for non-payment.

TDS rate:1% TDS is applicable if buying price or guidance value is more than Rs. 50 Lakhs, whichever is higher. TDS is applicable for residential property, commercial property and land. But this does not include agricultural land.

TDS for NRIs is different because the government deducts capital gains and TDS for the NRIs. Below is the TDS rate for NRIs

When to pay TDS:Buyer needs to pay TDS on or before registering the sale deed, as the registering officer verifies the TDS challan before proceeding sale deed registration, also It is important to mention TDS Challan number in sale deed.

Details required to pay TDS:The buyer does not require a TAN. When filling the Form 26QB, submit the names, addresses, PAN, phone number and email id of both the buyer and the seller.

Submit the complete address of scheduled property (to be purchased), the date of the agreement, the date of the payment, and the buying price. Make TDS payments online via net banking or physically at the bank. If there is more than one buyer or seller, need to furnish the details of each party in Form 26QB

Pay your TDS here e-Filing Home Page, Income Tax Department, Government of India

7. Registration of Sale Deed

The sale deed is an instrument in writing that transfers the ownership of the property. Registration of the property is the final step in the process as registration implies that the buyer (in whose name property is registered) is the lawful owner of the property with all rights, obligations, and duties towards the same. The objective of registration is to prevent fraud and dispute at the same time maintaining public records for the same. The immovable property can be registered at sub-registrar’s office within whose jurisdiction the property falls.

The stamp duty is levied on the value of buying price or guidance value, whichever is higher. Below is the total government charge for resale flat

- Stamp Duty & Surcharge: 5.1% of buying price or guidance value, whichever is higher

- Registration: 1% of buying price or guidance value, whichever is higher

- Cess: 0.5% of buying price or guidance value, whichever is higher

- Scanning: Rs. 35 per page

Please note that 0.5% stamp duty paid for sale agreement franking shall be adjusted at the time of registration of sale deed in stamp duty, provided you bring the original sale agreement to the sub-registrar office (you would need to get it from your banker in case of home loan availed). This process is called DENOTE process and is not applicable in assignment / swapping cases.

Documents required for Sale Deed registration:

- Parent Deed

- Seller’s sale deed

- Tax paid receipt (Current financial year)

- eKhata

- Occupation certificate

- Sale Agreement

- Printed sale deed (to be registered)

- TDS Challan

- Aadhar(Seller & Buyer)

- Active mobile phone for OTP Authentication

- Two Witnesses and their Aadhaar

8. MODT: (Memorandum of Deposit of Title Deed)

Memorandum of Deposit of Title Deed or MODT is applicable for all home loan borrowers.

It is essentially an undertaking given by you that you are depositing title documents of the property with the bank at your own free will in return for a loan.

Following are title documents deposited in bank under MODT

- Mother deed

- Sale deed

- Sale Agreement

- Encumbrance certificate

- Tax paid receipt

- Khata

- Occupation certificate

- and additional documents applicable for land like RTC, layout plan, building plan, etc.

After MODT registration, bank’s name reflects in encumbrance certificate. In the below encumbrance certificate, we encircled the bank details for your reference.

Irrespective of MODT is registered or not, bank collects all the title documents, which include sale deed, sale agreement, and latest encumbrance certificate.

Below are the government charges for MODT registration

- Stamp duty: 0.5% of loan sanctioned amount

- Registration: 0.1% of loan sanctioned amount

- Scanning Rs. 35 per page

Bank’s representative presence is not required for MODT registration in sub-registrar office.

Usually, MODT is registered immediately after the sale deed registration in same sub-registrar office.

The registered MODT looks like below image:

Note: After the sale deed registration, it’s important to change the name in khata, property tax and utility bill. In order to do so you need photo copy of title documents, hence before you hand over the tile documents to bank, take the scan copy of mother deed, sale deed and seller’s khata.

This completes the procedure to buy resale flat in Bangalore.

In Bangalore. we provide end-to-end assistance to buy resale property. To opt for our service, please write to us pgnproperties@gmail.com or WhatsApp to + 9 1 – 9 7 4 2 4 7 9 0 2 0 .

Thank you for reading…